They require a sacrifice of economic benefit in the future. The formula defines the relationship between a business’s Assets, Liabilities and Equity. At any moment in time the Accounting Equation must balance. For the past 52 years, Harold Averkamp (CPA, MBA) hasworked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com. To learn more about the balance sheet, see our Balance Sheet Outline.

We will now consider an example with various transactions within a business to see how each has a dual aspect and to demonstrate the cumulative effect on the accounting equation. The combined balance of liabilities and capital is also at $50,000. As business transactions take place, the values of the accounting elements quality operations manager change. The accounting equation nonetheless always stays in balance. When analyzed over time or comparatively against competing companies, managers can better understand ways to improve the financial health of a company. Accounts within this segment are listed from top to bottom in order of their liquidity.

The accounting method under which revenues are recognized on the income statement when they are earned (rather than when the cash is received). We could also use the expanded accounting equation to see the effect of reinvested earnings ($419,155), other comprehensive income ($18,370), and treasury stock ($225,674). We could also look to XOM’s income statement to identify the amount of revenues and dividends the company earned and paid out. At the same time, it incurred in an obligation to pay the bank.

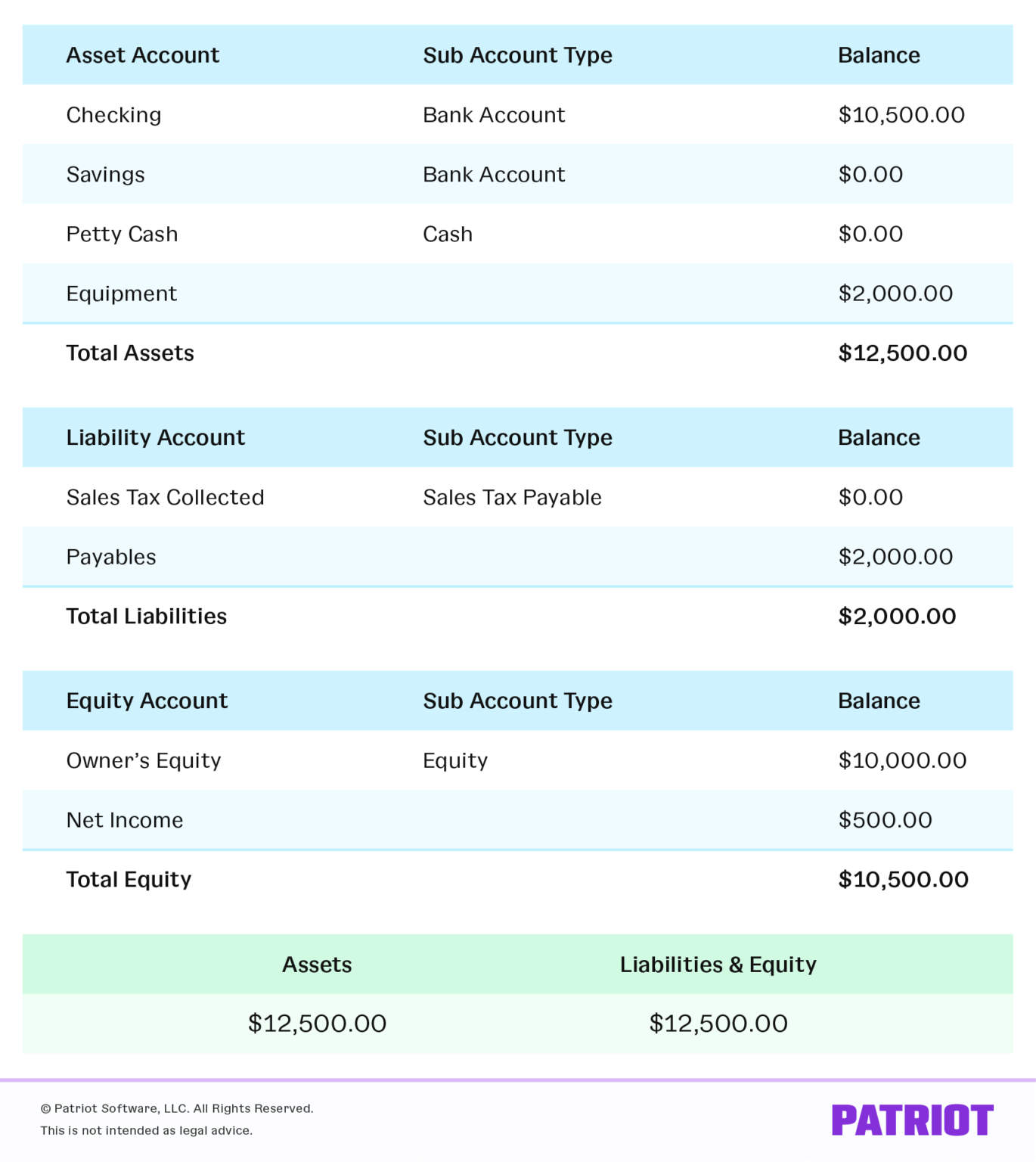

The assets should always equal the liabilities and shareholder equity. This means that the balance sheet should always balance, hence the name. If they don’t balance, there may be some problems, including incorrect or misplaced data, inventory or exchange rate errors, or miscalculations. The income statement and statement of cash flows also provide valuable context for assessing a company’s finances, as do any notes or addenda in an earnings report that might refer back to the balance sheet. On the balance sheet, the assets side represents a company’s resources with positive economic utility, while the liabilities and shareholders equity side reflects the funding sources.

A balance sheet must always balance; therefore, this equation should always be true. Balance sheets are typically prepared and distributed monthly or quarterly depending on the governing laws and company policies. Additionally, the balance sheet may be prepared according to GAAP or IFRS standards based on the region in which the company is located. Simply put, the rationale is that the assets belonging to a company must have been funded somehow, i.e. the money used to purchase the assets did not just appear out of thin air to state the obvious. To learn more about the income statement, see Income Statement Outline. Accountingo.org aims to provide the best accounting and finance education for students, professionals, teachers, and business owners.

Once you get the loan, this is how your accounting equation changes. Depending on the company, different parties may be responsible for preparing the balance sheet. For small privately-held businesses, the balance sheet might be prepared by the owner or by a company bookkeeper.

Employees usually prefer knowing their jobs are secure and that the company they are working for is in good health. That’s because a company has to pay for all the things it owns (assets) by either borrowing money (taking on liabilities) or taking it from investors (issuing shareholder equity). A balance sheet is one of the primary statements used to determine the net worth of a company and get a quick overview of its financial health.

For this reason, a balance alone may not paint the full picture of a company’s financial health. In short, the balance sheet is a financial statement that provides a snapshot of what a company owns and owes, as well as the amount invested by shareholders. Balance sheets can be used with other important financial statements to conduct fundamental analysis or calculate financial ratios. Below liabilities on the balance sheet is equity, or the amount owed to the owners of the company. Since they own the company, this amount is intuitively based on the accounting equation—whatever assets are left over after the liabilities have been accounted for must be owned by the owners, by equity.

In accounting, the claims of creditors are referred to as liabilities and the claims of owner are referred to as owner’s equity. Before explaining what this means and why the accounting equation should always balance, let’s review the meaning of the terms assets, liabilities, and owners’ equity. Essentially, the representation equates all uses of capital (assets) to all sources of capital, where debt capital leads to liabilities and equity capital leads to shareholders’ equity. The accounting equation is also called the basic accounting equation or the balance sheet equation. At the bottom of the balance sheet, we can see that total liabilities and shareholders’ equity are added together to come up with $375,319 billion which balances with Apple’s total assets.

Comments