As with FIFO, if the price to acquire the products in inventory fluctuates during the specific time period you are calculating COGS for, that has to be taken into account. To calculate the Cost of Goods Sold (COGS) using the LIFO method, determine the cost of your most recent inventory. LIFO, or Last In, First Out, is an inventory value method that assumes that the goods bought most recently are the first to be sold.

The example above shows how a perpetual inventory system works when applying the FIFO method. The wholesaler provides a same-day delivery service and charges a flat delivery fee of $10 irrespective of the order size. Bill sells a specific model of a toaster on his website for $12 apiece.

Companies with perishable goods or items heavily subject to obsolescence are more likely to use LIFO. Logistically, that grocery store is more likely to try to sell slightly older bananas as opposed to the most recently delivered. Should the company sell the most recent perishable good it receives, the oldest inventory items will likely go bad. The how to start a bookkeeping business 2023 guide valuation method that a company uses can vary across different industries. Below are some of the differences between LIFO and FIFO when considering the valuation of inventory and its impact on COGS and profits. Also, through matching lower cost inventory with revenue, the FIFO method can minimize a business’ tax liability when prices are declining.

The remaining two guitars acquired in February and March are assumed to be unsold. Because the value of ending inventory is based on the most recent purchases, a jump in the cost of buying is reflected in the ending inventory rather than the cost of goods sold. In a period of inflation, the cost of ending inventory decreases under the FIFO method. Our understanding of labor organizations and our daily involvement gives us the unique ability to be a resource to enable Executive Boards and governing bodies in making informed decisions. Regardless of your craft or jurisdiction, we possess the knowledge and resources to handle your accounting needs.

Higher reported gross income also leads to an inflated representation of profits. A company generates the same amount of income and profits regardless of whether they use FIFO or LIFO, but the different valuation methods lead to different numbers on the books. This can make it appear that a company is generating higher profits under FIFO than if it used LIFO. Higher inflation rates will increase the difference between the FIFO and LIFO methods since prices will change more rapidly. If inflation is high, products purchased in July may be significantly cheaper than products purchased in September.

Theoretically, the cost of inventory sold could be determined in two ways. One is the standard way in which purchases during the period are adjusted for movements in inventory. The second way could be to adjust purchases and sales of inventory in the inventory ledger itself. The problem with this method is the need to measure value of sales every time a sale takes place (e.g. using FIFO, LIFO or AVCO methods). If accounting for sales and purchase is kept separate from accounting for inventory, the measurement of inventory need only be calculated once at the period end. This is a more practical and efficient approach to the accounting for inventory which is why it is the most common approach adopted.

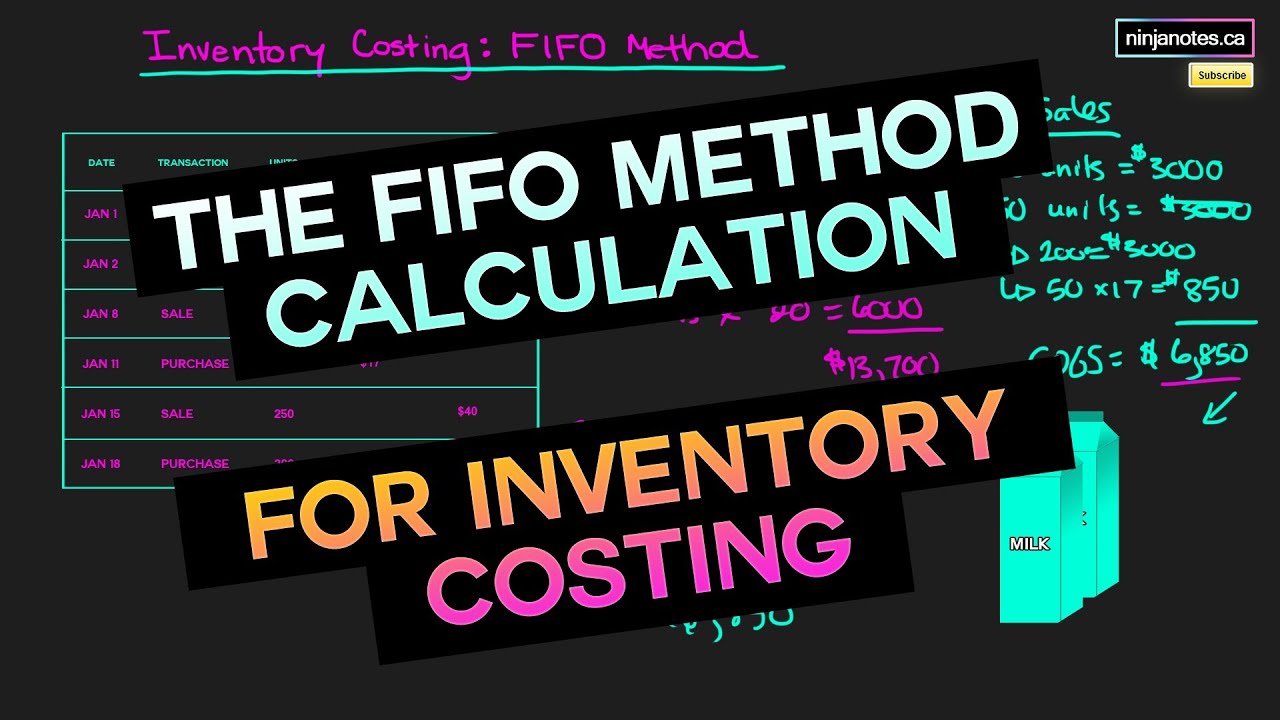

If the number of units sold exceeds the number of oldest inventory items, move on to the next oldest inventory and multiply the excess amount by that cost. Assuming that prices are rising, this means that inventory levels are going to be highest as the most recent goods (often the most expensive) are being kept in inventory. This also means that the earliest goods (often the least expensive) are reported under the cost of goods sold. Because the expenses are usually lower under the FIFO method, net income is higher, resulting in a potentially higher tax liability. In periods of falling inventory costs, a company using FIFO will have a lower gross profit because their cost of goods sold is based on older, more expensive inventory.

Jeff is a writer, founder, and small business expert that focuses on educating founders on the ins and outs of running their business. Consider the following practices to ensure your FIFO calculations are accurate and up to date. Inventory is valued at cost unless it is likely to be sold for a lower amount.

11 Financial may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Finance Strategists has an advertising relationship with some of the companies included on this website. We may earn a commission when you click on a link or make a purchase through the links on our site.

Comments